Newsletter

|

Aug 21, 2025

Risk-On in the Face of Uncertainty explores why younger Americans embrace gambling, crypto, trading, and side hustles as traditional wealth paths erode.

Copy Link

.webp)

In the United States, there seems to be a growing feeling (amongst some/many) that the American dream is slipping away. For about three decades, the Wall Street Journal conducted a survey asking people if they believe “life for their children’s generation will be better than it has been for their own”.

In 2023, 78% of Americans surveyed responded they “do not feel confident” that will be the case. This is the highest number since the survey was started.

This week we want to hone in on some of the potential reasons for this pessimistic view, and how we believe consumers are increasing their risk appetite to try to take back control.

Geopolitical tension, wars, political unrest, or even a dystopian AI future, could all play a role in why people feel that tomorrow may be worse than today, but we believe a large factor is likely financial strain. In the same WSJ article, 44% of respondents said their financial situation was “in worse condition than expected”. While wars abroad are certainly a cause for concern, the state of our wallets hit very close to home.

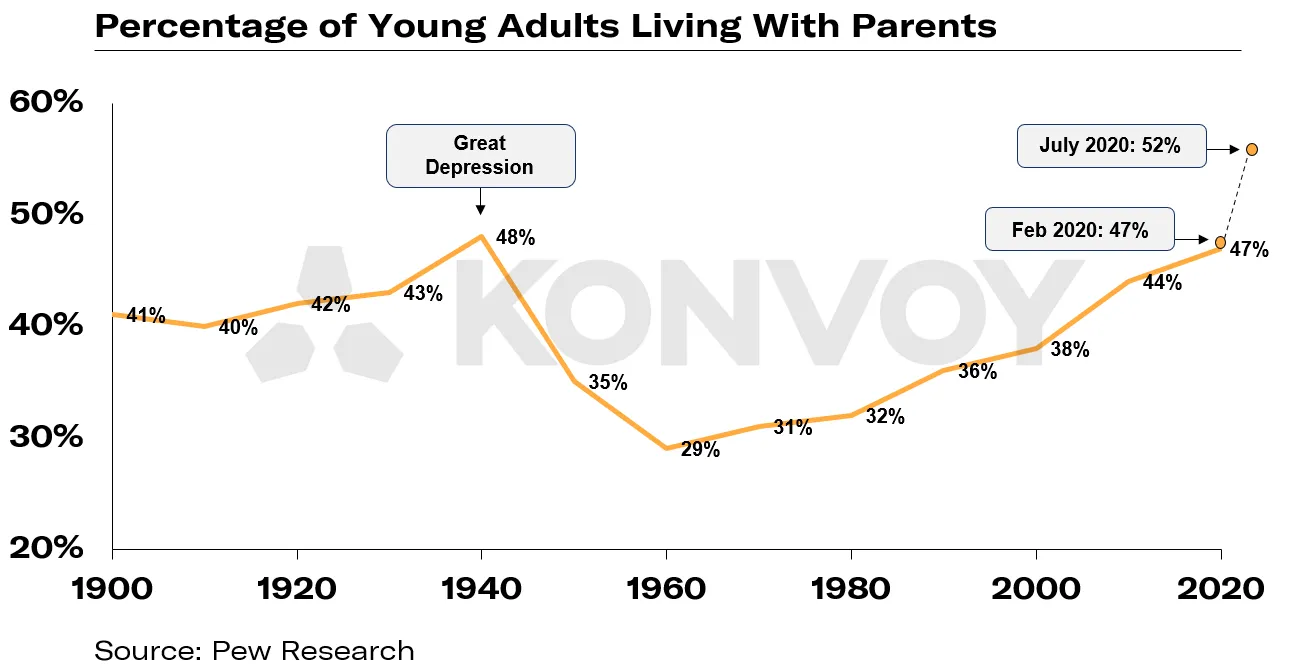

This sensation that we are falling behind financially is likely the largest reason driving the feeling that the American dream feels harder to achieve. While the pandemic saw a spike in young adults living with their parents, this has been a trend that has been evolving since the 1960s and has recently surpassed the previous peak seen during the Great Depression (Pew Research).

Similarly, over half of Gen Z reported that they don’t make enough money to live the life they want, pointing to high cost of living as one of the main challenges (BofA). This concern is exhibited by the ratio between home prices and income over time. In 1990, the ratio was about ~3:1 in the United States, this has increased to ~4:1 in 2023 (NPR).

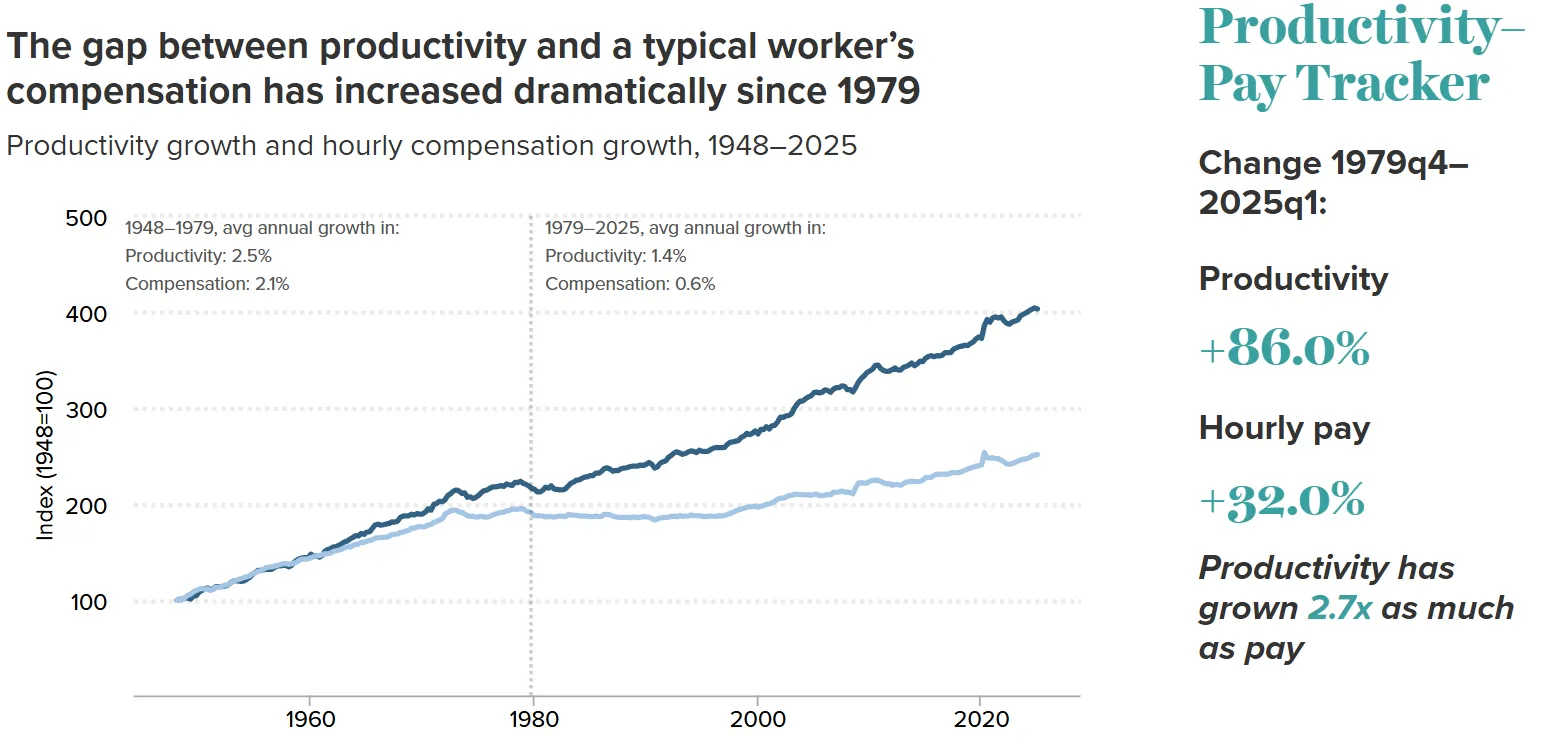

Despite an increase in productivity, wages have not kept pace.

Muted wage growth, people living with their parents, and high cost of living are making it hard to envision a brighter future.

We believe that the “risk-on” mentality being exhibited by younger consumers today can at least be partially driven by these pressures. Many consumers, especially young people, are likely thinking: “If I cannot get to where I want to go with my day job, I might as well roll the dice.” We believe this train of thought explains a handful of recent trends in the consumer space:

Sports gambling is a high-risk activity that has been growing at an incredible rate. As a proxy for the industry, DraftKings has been growing at >70% CAGR since 2019 (DraftKings).

The whole sweepstakes betting industry has recently evolved to provide access to betting where traditional sports betting is not allowed.

This market has also grown rapidly and is expected to do $11bn in revenue in 2025. The market for “alternative” betting platforms has also exploded as a way to scale at a pace unhindered by stagnant regulatory frameworks (more on this topic here: Sports Betting: Take A Gamble)

A slightly more sophisticated version of this “risk-on” phenomenon is retail trading, where non-institutional investors (often referred to as “retail investors”, like you and I) place personal bets on the stock market. A proxy here is Robinhood’s revenue which has grown at a ~60% CAGR since 2019. Robinhood's 2024 revenue just surpassed its previous 2021 COVID peak (Robinhood).

This is both a risk-on asset and is viewed by some as a proxy for hedging against political instability. While not entirely retail focused, Coinbase’s revenue could be used as a proxy for growth here: since 2019, revenue has also increased at a ~70% CAGR (Coinbase).

We don’t view the growth of these industries as a coincidence. Each of them, while extremely risky, comes with the promise of something more – a way to move out of your parents house, a way to buy a home, or even a small increase in monthly income.

Unless some of the macro issues begin to subside, we expect consumers to continue to maintain a risk-on appetite (even if that sounds counter-intuitive in a tougher macro environment for the consumer). This may be a headwind for many legacy industries including traditional financial services, insurance, or even higher-education, but we expect a few other industries to benefit:

A generation that feels locked out of traditional wealth-building is embracing higher-risk, higher-reward behaviors across finance, gaming, and lifestyle choices. Unless affordability improves and macro pressures ease, we expect this “roll the dice” mindset to persist, benefiting industries built on volatility and upside.

.png)

.jpg)

.jpg)

.png)

.png)

.png)

.png)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)